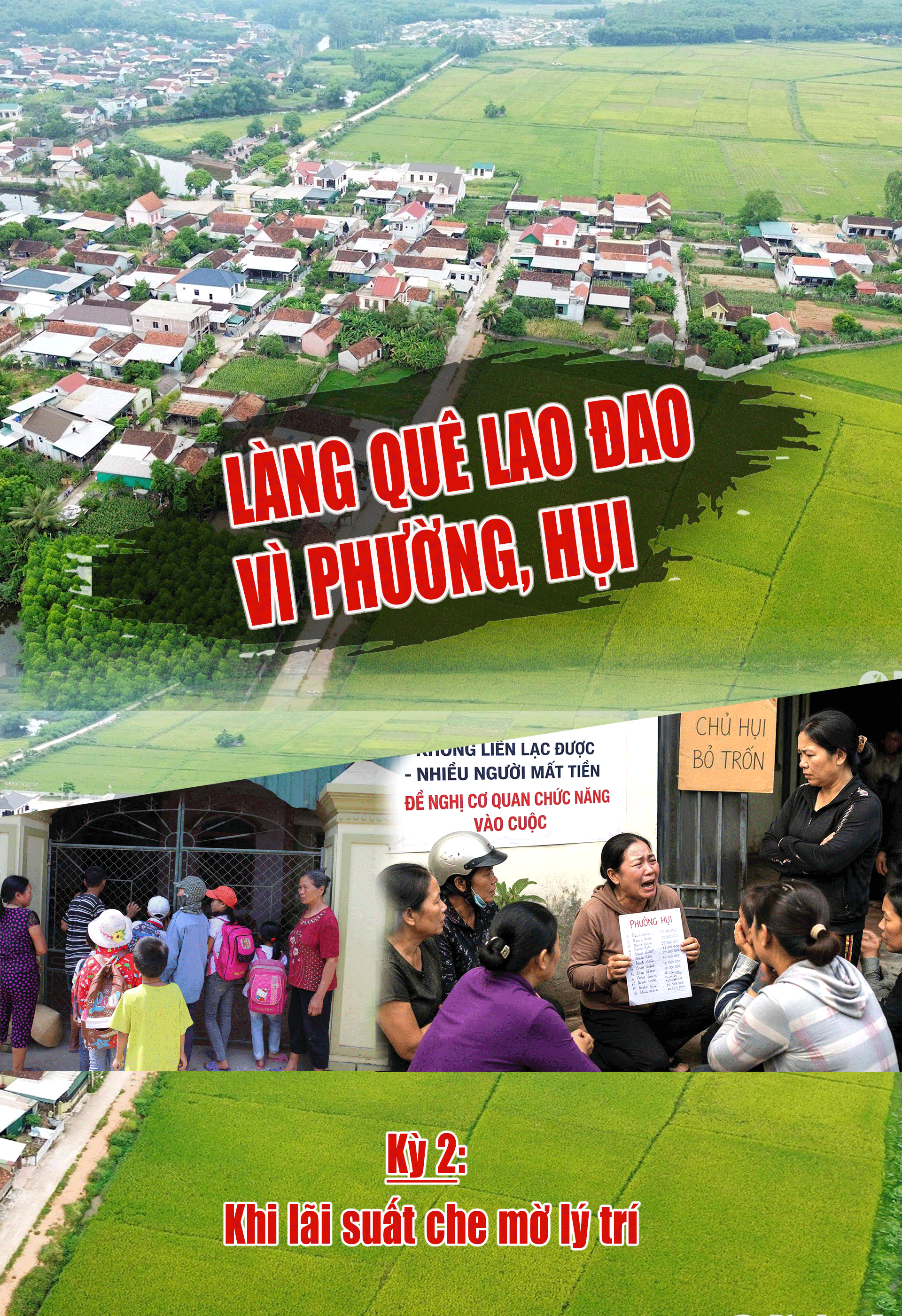

Rural villages in turmoil due to informal lending schemes - Part 2: When interest rates cloud judgment.

Promises of "quick profits, early cash receipts" led many people in Tan Ky commune to join informal lending groups with high expectations. But as the profit margins increased, so did the risks. When the group leaders collectively announced the cessation of operations, many were shocked to realize that their greed and blind trust had trapped them in a financial snare with no way out.

Content: Tien Hung /Present:Tran HaiApril 29, 2026

Promises of "quick profits, early cash receipts" led many people in Tan Ky commune to join informal lending groups with high expectations. But as the profit margins increased, so did the risks. When the group leaders collectively announced the cessation of operations, many were shocked to realize that their greed and blind trust had trapped them in a financial snare with no way out.

.png)

For over a month now, Mrs. Nguyen Thi Hau (54 years old) and her husband, residing in Tan Ky commune, have been living in constant anxiety. They don't know when they'll be able to recover the nearly 1.8 billion VND they invested in informal lending schemes. Meanwhile, dozens of people frequently gather at the scheme's owner's residence, hoping to pressure him into returning the money.

Ms. Hau recounted that she met Ms. Hoang Thi Qu. (36 years old), from the same Tan Ky commune, through trading and was invited to join a charity group about a year ago. “I trusted her because I saw that she lived a very luxurious life and often updated pictures of herself doing charity work on social media. Who would have thought…,” Ms. Hau said.

Ms. Hau participated in a total of 16 "ward networks," also known as "ward groups," operating through chat groups with approximately 300 members. Every day, the group leader would announce which groups were starting operations that day, and anyone who registered would be added to a private group to receive notifications and pay fees. The duration of these groups was flexible, ranging from 5, 7, 10 to 15 days, and the number of participants was not fixed.

A typical lottery scheme has 8 members, each contributing 20 million VND per week. In the first week, an additional 10% is paid as a "fee" to the scheme's organizer. This means that those who draw their numbers for the first time will not receive any interest, while the organizer receives the 16 million VND "fee." In the following week, those who have already drawn their numbers must pay 22 million VND, while those who haven't drawn yet only pay 20 million VND. This continues until the last person to draw their number receives the highest interest.

Accordingly, after only 8 weeks, with this lottery scheme, Ms. Hau would receive 12 million VND in interest. However, after paying a total of 142 million VND for 7 weeks in one scheme, when it was almost her turn to receive the money, Ms. Hau received a notification that the scheme had stopped operating. Similarly, another lottery scheme worth 50 million VND/15 days with 6 members. Ms. Hau registered as the last person to draw a prize to receive an additional 20 million VND in interest (after only 3 months). However, after she had paid 5 installments totaling 255 million VND, the system stopped.

"I knew that high returns meant high risks, but seeing others making quick profits, I couldn't resist. The returns were so high that everyone wanted to be the last to get more. I was no different," Ms. Hau admitted. But that very choice turned them into the ones bearing the greatest risk.

After several rounds of payments, just as they were waiting for their turn to receive their winnings, the lottery operators suddenly announced they were ceasing operations. Those who had already received their money earlier were left with the entire loss, while those who paid last, like Mrs. Hau, bore the brunt of the losses. In one lottery scheme alone, she had paid 142 million VND, only for it to collapse. Another scheme lost 255 million VND. In total, across 16 schemes, the amount lost reached nearly 1.8 billion VND – almost the entire family's assets.

.png)

Similarly, Ms. Le Thi Huong (40 years old), from Tan Ky commune, said that because she saw the high interest rate and trusted Ms. Hoang Thi Qu., she participated in 14 informal lending schemes and paid nearly 1 billion VND to Ms. Qu. Like Ms. Hau, Ms. Huong registered to be the last to receive the money to enjoy a higher interest rate, but the scheme ceased operations before she could receive the money.

Notably, during the operation of these neighborhood watch groups, the group leader also implemented many strict regulations, such as a fine of 500,000 VND if members paid late after 9 PM, and a fine of 1 million VND per day for even later payments.

According to Ms. Huong, at least 22 people have filed complaints against ward head Hoang Thi Qu. for embezzlement totaling over 13 billion VND, but the actual amount could be higher.

Regarding the reason for the suspension of operations, on the afternoon of February 24, 2026, Ms. Hoang Thi Qu. informed the members in the group chat that due to "unexpected circumstances," the head of the lottery group had to temporarily suspend operations until March 1st. However, on March 1st, the head of the lottery group announced again that due to too many people being unable to pay, the lottery group would cease all operations. Many members then went to the head of the lottery group's house and were told that because many people had already drawn lots but stopped paying, the head of the lottery group no longer had money to pay those who hadn't. Not long after, valuable assets of the head of the lottery group, such as a car, were transferred to relatives, further angering the lottery group members.

According to the victims, after the savings scheme ceased operations, the members sat down together and discovered many irregularities in its operation. “To be honest, the high interest rates blinded our judgment. If we thought carefully, we could understand that with such a scheme, no one would be foolish enough to take out the first installment and then have to pay high interest to those who took out the last installment. It could only be a fake account,” said Ms. Nguyen Thi Hau.

According to Ms. Hau, in all the online lending groups she participated in, as well as those of other victims, there were always nine very strange social media account names. These people were of unknown origin, and no one knew them. However, the names of these individuals appeared in almost all the groups and were pre-selected by the group leader. “Every time it was time to pay, only I took pictures of the money transfer receipts and sent them to the group, while these people only sent symbols; no one sent a receipt to the group. Such an unusual situation should have been noticed earlier. Now I realize that, over the past period, only I was actually transferring money in the group, while the other members were likely fake,” Ms. Hau stated.

Alarmingly, after one informal lending group collapsed, many others also ceased operations simultaneously, creating a chain reaction that left hundreds of people penniless. Money that seemed like "quick profits" has now become a heavy burden of debt. Many families are experiencing conflict and discord, and some even face the risk of breaking up.

The story in Tan Ky commune illustrates a reality: When profits exceed the normal level, it's no longer an opportunity, but very likely a trap. In those informal lending schemes, no one thinks they will be the ones to suffer losses. But when the cycle stops, the risk always falls on those who joined later – those who bet the most. High interest rates can cloud judgment for a moment. But the price paid, for many, lasts for years afterward.

Lawyer Le Anh from the Nghe An Provincial Bar Association stated that, according to information provided by the public in this case, the ringleader established numerous organized gambling rings through social media, with each ring averaging 9-15 members. Of these, only 1-2 members actually participated in the gambling, while the remaining members were not involved but were merely registered by the ringleader.

“These people are called virtual members. They have some kind of debt relationship with the group leader, or something similar, that the group leader requires these 'virtual members' to register in the group, leaving the rest to the group leader. The group leader's purpose is to make real players believe that the group is operating normally. And real players are always arranged to be the last to receive the group, and when they receive it, the group leader declares the group bankrupt,” said lawyer Le Anh.

According to the lawyer, in online community groups on social media, virtual members only confirm that they have paid or received money through text messages. Meanwhile, real community members must take a picture of the transfer receipt and send it to the group leader for confirmation. These are prominent elements demonstrating deceptive tactics aimed at making real community members believe that the group is operating normally and making regular payments. Then, when they are the final recipients, the group leader announces that the group has collapsed,” lawyer Le Anh stated.

Mr. Le Viet Quy, Vice Chairman of the Tan Ky Commune People's Committee, said that the Commune Party Committee has been informed of the incident and has issued a directive to the secretaries of the subordinate Party branches to widely disseminate information to cadres and Party members to raise awareness and correctly understand the regulations of the law on credit management and currency trading, and absolutely not to participate in illegal informal lending schemes. They are also to educate relatives and the local community to have a correct understanding, to avoid being deceived or lured, and to prevent financial losses. The Tan Ky Commune Party Committee also requested the Commune Police Party Committee to direct the investigation and gather information on the incident; verify relevant information, and advise on handling the matter according to the law. At the same time, they directed the ensuring of security and order in the area…

Meanwhile, Major Nguyen Trong Han, Deputy Head of Tan Ky Commune Police, said that the unit had received information that many people had participated in a rotating savings and credit association (ROSCA), after which the ROSCA leader announced the cessation of operations. Immediately afterward, the unit promptly reported the matter to the Provincial Police and the Criminal Police Department for verification and investigation.

-------o0o--------

(To be continued)