Vietnamese people are borrowing and spending beyond their means.

According to Rồng Việt Securities Company (VDSC), Vietnamese people are overly optimistic about future income, leading them to readily take on more expenses and borrow more for current spending.

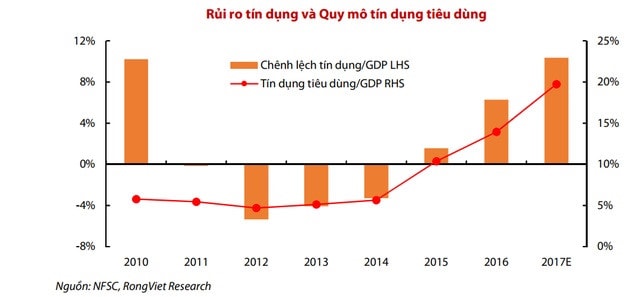

A report by VDSC provides statistics on consumer credit growth in Vietnam. According to the report, the increase was nearly 60% in 2017, and it forecasts an average annual growth rate of 29-30% for consumer loans over the next three years.

People are borrowing more.VDSC assesses that in the short term, the growth potential in this sector remains very wide open, as the scale of consumer credit was only about 19% of GDP in 2017. This capital flow will create momentum for the overall demand of the economy and positively impact GDP growth in the coming years, supporting the recovery of the Vietnamese real estate and stock markets.

However, financial risks are also increasing as households become more open to spending and borrowing, given the relatively low savings rate compared to other countries in the region.

|

By 2016, Vietnam's savings rate was only 29% of GDP, quite low compared to other countries in the region. Based on consumer behavior trends, VDSC observes that people are overly optimistic about their future income and are willing to compromise and borrow more for current spending.

According to VDSC's assessment, this raises concerns about people's ability to repay their debts. Furthermore, if increased consumer spending is not linked to economic growth, the health of the economy will weaken in the long term.

Lessons from around the worldVDSC also believes that household debt growth and asset price movements have a two-way interaction, based on historical lessons from countries around the world.

Since the 2008 financial crisis, home prices in Canada and the United States have differed significantly. While the US home price index has fallen nearly 25% since its mid-2008 peak, home prices in Canada have generally maintained a long-term upward trend.

One of the key reasons is the difference in credit flows into the household sector. Conversely, when real estate assets appreciate in value and are used as collateral, it improves the credit picture for households. Therefore, households tend to proactively use personal financial leverage.

VDSC also noted the lessons from China, where most experts are concerned about an asset bubble. There is a strong positive correlation between the rate of increase in housing prices in major cities and the rate of increase in household debt in China.

|

| Illustrative image |

The story in Vietnam

Given the developments in the Vietnamese market, housing and office prices have shown a clear recovery over the past nearly five years.

As of the second quarter of 2017, the housing price index in Ho Chi Minh City reached 93 points, a 5.1% increase compared to the 2014 low. Meanwhile, the office price index was recorded at 89 points, a significant 23.1% increase compared to the beginning of 2013.

There are many reasons to explain this recovery, but VDSC believes that the flow of credit capital is one of the key factors.

Thus, there is still ample room for growth in consumer credit, which will have a positive impact on the economy in the medium term.

However, the inherent risks cannot be ignored, as more than 50% of consumer credit flows into real estate, a major driving force supporting the market's recovery. This contributes to distortions in the calculation and published data regarding real estate credit flows.

According to VDSC's assessment, this development also poses risks as these assets are used as collateral and banks overestimate the creditworthiness of borrowers.